Memory Is Not One Trade

What are the chokepoints along the memory supply chain?

The obvious way to invest in high-bandwidth memory is to buy the DRAM suppliers. That’s not wrong.

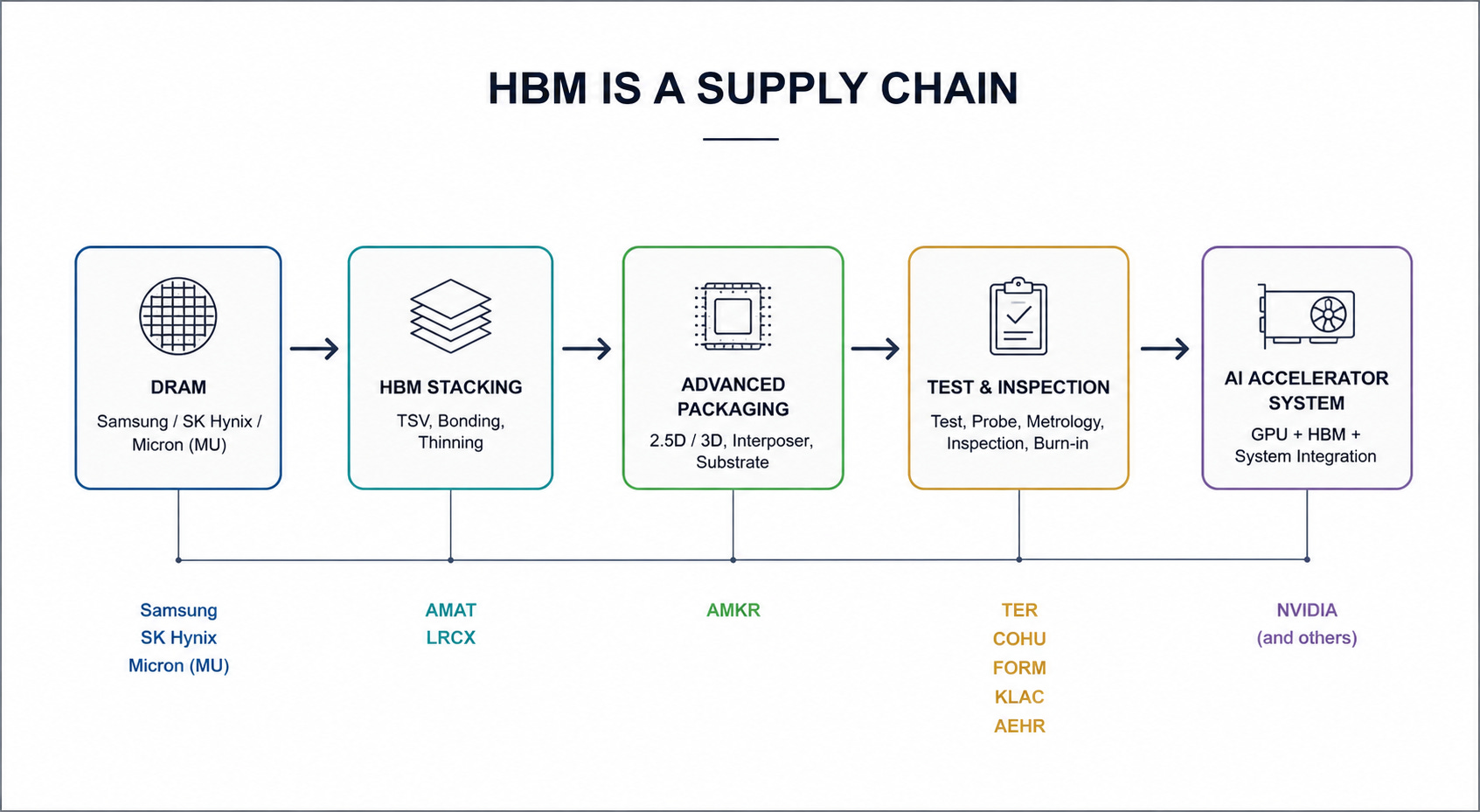

High bandwidth memory (HBM) is effectively a three-company market: SK Hynix, Samsung, and Micron.

Depending on the quarter, those three companies control more than 95% of global DRAM production. In HBM specifically, SK Hynix has emerged as the early leader, Micron is ramping aggressively, and Samsung is investing heavily to regain share.

The numbers explain why investors are paying attention. Industry analysts estimate the HBM market was roughly $4–5 billion in 2023 and may approach $30–40 billion annually before the decade ends. Few semiconductor categories can grow at that pace.

But the better question is: What is the supply chain trade here?

Let’s look at the progression. Nvidia’s H100 shipped with 80GB of HBM3 and roughly 3.35TB/s of memory bandwidth. The H200 jumped to 141GB of HBM3e and 4.8TB/s. Nvidia’s Blackwell Ultra platform pushes to 288GB of HBM and approximately 8TB/s of bandwidth.

This is a 3.6x increase in memory capacity and a 2.4x increase in bandwidth in just a few product generations.

The economics are equally striking. Industry estimates suggest HBM can account for 20–30% of the bill of materials of a leading AI accelerator. A single HBM stack can cost hundreds of dollars. A fully populated AI GPU package may contain thousands of dollars of memory.

The reason is simple. AI workloads are increasingly constrained by data movement.

GPUs can perform mathematical computations. The challenge is feeding them tokens, weights, activations, embeddings, and KV cache data fast enough to keep utilization high. Every increase in model size, context window, inference volume, and agent activity pushes against the same bottleneck: memory bandwidth.

HBM is the toll booth. And the toll booth is becoming more valuable every year. So companies like Micron, Samsung, and SK Hynix matter a lot.

Micron expects HBM revenue to exceed several billion dollars annually within the next few years. SK Hynix has reportedly secured a dominant share of Nvidia’s HBM supply and has publicly discussed selling out much of its HBM capacity well in advance. Samsung remains one of the largest memory manufacturers on earth, generating tens of billions of dollars annually from memory products and investing aggressively to close the gap.

These 3 companies are the first-order beneficiaries of the AI memory bottleneck. But HBM is not just DRAM stacked vertically.

Modern HBM stacks contain up to 12 memory dies connected through thousands of through-silicon vias (TSVs). Manufacturing requires wafer thinning, precision bonding, advanced packaging, thermal management, inspection, testing, and yield optimization.

A defect in one layer can compromise the entire stack. And even a perfect HBM stack is worthless if it cannot be integrated with the GPU. That pulls in the rest of the supply chain.

Applied Materials, Lam Research, and KLA sit upstream in deposition, etch, metrology, and inspection. These companies collectively generate more than $80 billion in annual revenue because semiconductor manufacturing increasingly depends on process precision. HBM amplifies that requirement.

As stack heights increase from 8-high to 12-high and beyond, defect costs rise dramatically. Yield becomes more valuable. Inspection becomes more valuable. Process control becomes more valuable.

Teradyne and Cohu benefit because memory testing becomes harder as bandwidth, density, and thermal loads increase. FormFactor matters because advanced probe cards are required to validate increasingly complex memory devices before packaging.

Aehr Test Systems is interesting because burn-in and reliability testing become more important when a single AI accelerator can cost $30,000–$40,000 and a rack can exceed $1 million.

Then there is packaging. This may be the most underappreciated bottleneck in AI infra. TSMC’s CoWoS advanced packaging technology has become one of the critical constraints in AI accelerator production. Industry estimates suggest CoWoS capacity has expanded several-fold since 2023, yet demand continues to outstrip supply. Amkor sits directly in this trend.

Advanced packaging is no longer a low-margin back-end service. It is becoming one of the highest-value manufacturing steps in the AI supply chain. Without packaging capacity, GPUs cannot ship regardless of how many wafers are produced.

This is the key observation here: When a bottleneck becomes strategic, value spreads sideways.

The market starts with: “Who sells HBM?”

Then it moves to: “Who enables HBM yield?”

Then: “Who tests it?”

Then: “Who packages it?”

Then: “Who supplies the tools, materials, substrates, and inspection systems?”

This is how a single bottleneck becomes an ecosystem. For VCs, the takeaway is even more important.

Should we invest in the next DRAM company? Perhaps not. That game requires tens of billions of dollars of capital expenditure and decades of process expertise.

Instead, build around the constraint. The opportunities are in yield analytics, thermal simulation, packaging design automation, memory-aware compilers, HBM test optimization, substrate inspection, supply-chain software, and infra tools that reduce memory pressure.

The most interesting startup wedge may be software that makes scarce HBM go further. A modern AI server can contain hundreds of gigabytes of HBM costing tens of thousands of dollars. Every percentage point of utilization matters.

Better KV-cache management

Smarter memory scheduling

Compression techniques that preserve model quality

Inference routing based on memory profiles

Profiling tools that identify wasted bandwidth

These solutions can create enormous value because they improve utilization of one of the most expensive resources in the AI stack.

HBM is becoming the scarce resource inside AI infra. But scarcity never stops at one component.

It propagates into every tool, process, machine, material, workflow, and software layer required to manufacture, test, package, and use that component efficiently.

If you are getting value from this newsletter, consider subscribing for free and sharing it with 1 infra-curious friend: